Greystone Logistics is a US company producing recycled plastic pallets. Its headquarters are located in Oklahoma. It is a microcap traded on OTC QB market.

This company has been selling for some years now pallets that are made out of recycled plastic, being more ecological and lighter than classical wood pallets.

I found this opportunity because of cheap ratios and then I found some nice older analysis here (2+2 forum) and here (Nonamestocks). I advise you to read especially this last one, you will find a ton of information. My thesis is still the same and stays simple : buying growth at a cheap price.

I built my position in May 2020 and added some dollars recently.

Financial Ratios:

Market Cap (in USD) = 38M

Price to Book = 4

Price to Sales = 0.6

EV/EBITDA = 4.9

PER = 10

PEG = 0.26

Total Debt/Equity = 200%

Return on Equity = 55%

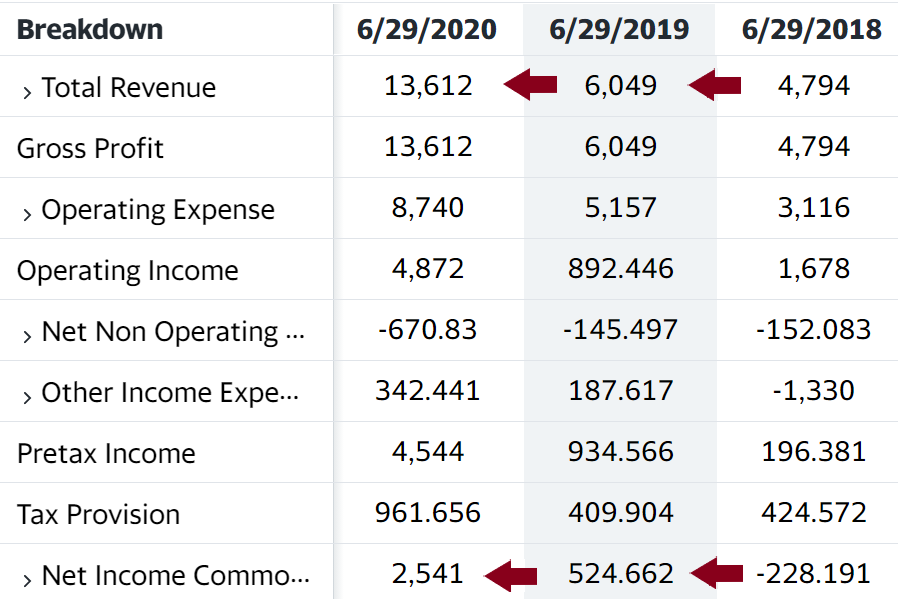

Sales have been growing at a nice rhythm these last years :

In 2020, sales were $76.2M with a $11.4M gross profit despite the covid crisis impacting negatively the activity.

And the best part (last year is 2020 below) :

The conclusion is pretty simple: we have a super cheap growth but a high level of debt. Provided that the earning growth stays the same in the future, the debt level is tolerable.

Chart

Nothing to say here, the dip in 2020 was caused by COVID-crisis.

Risk

The company is in a niche market, a competitor could appear and take its place on the market, clients can change their mind towards plastic pallets or wood price can go down.

The recent increase in the wood price is a good catalyst for the company that will be more competitive on the market.

Disclosure : Long, bought at $0.89 in may 2020 and added some last week.

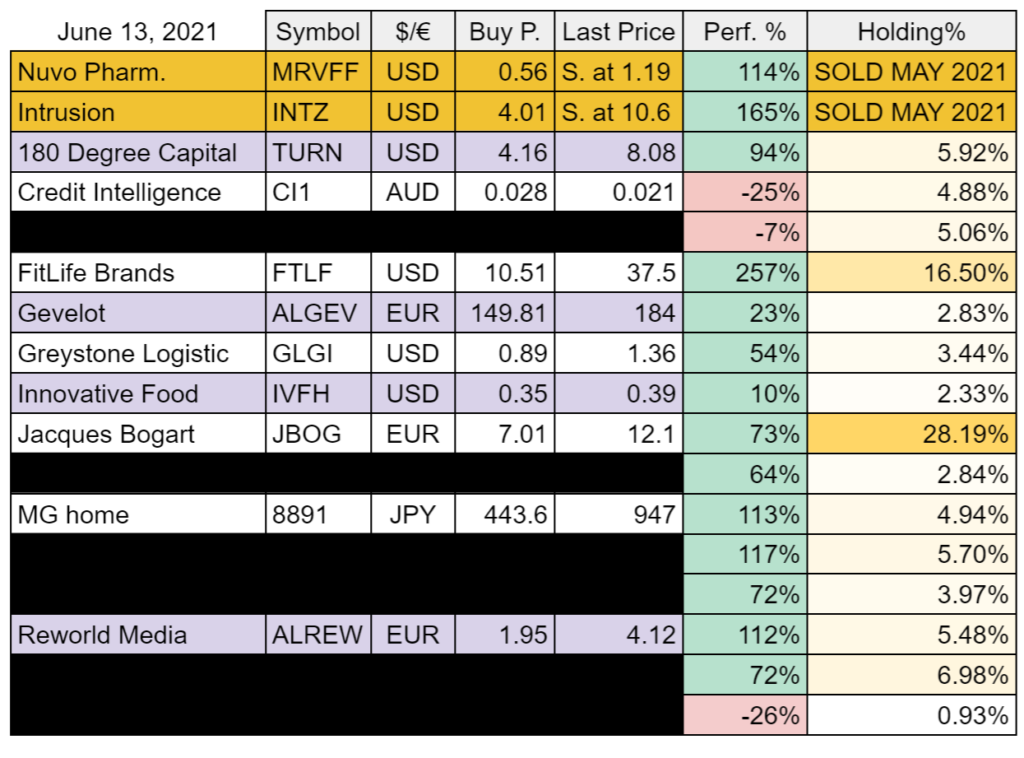

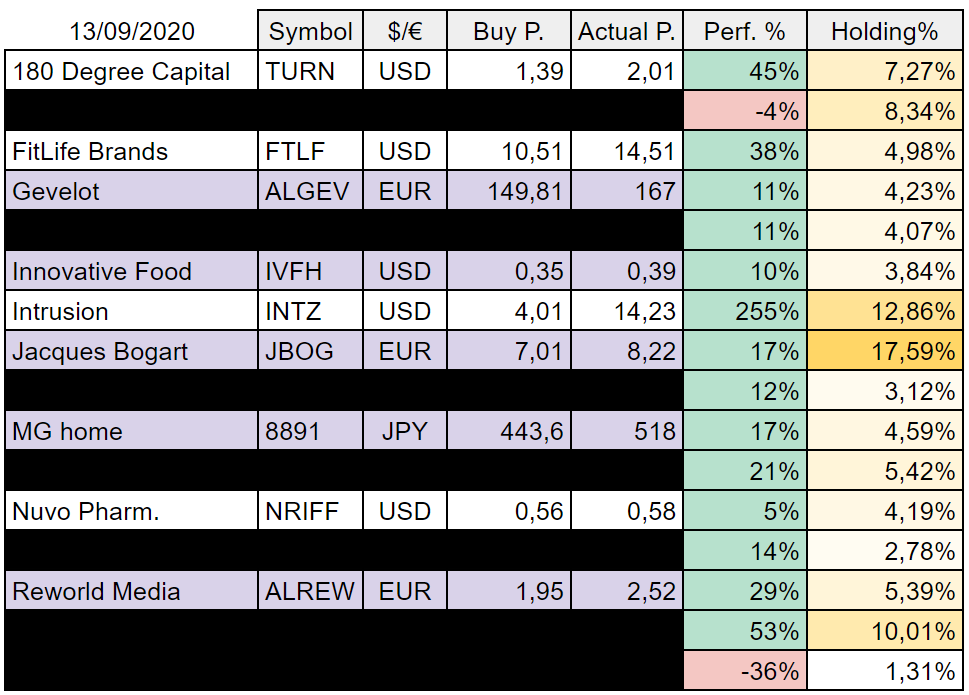

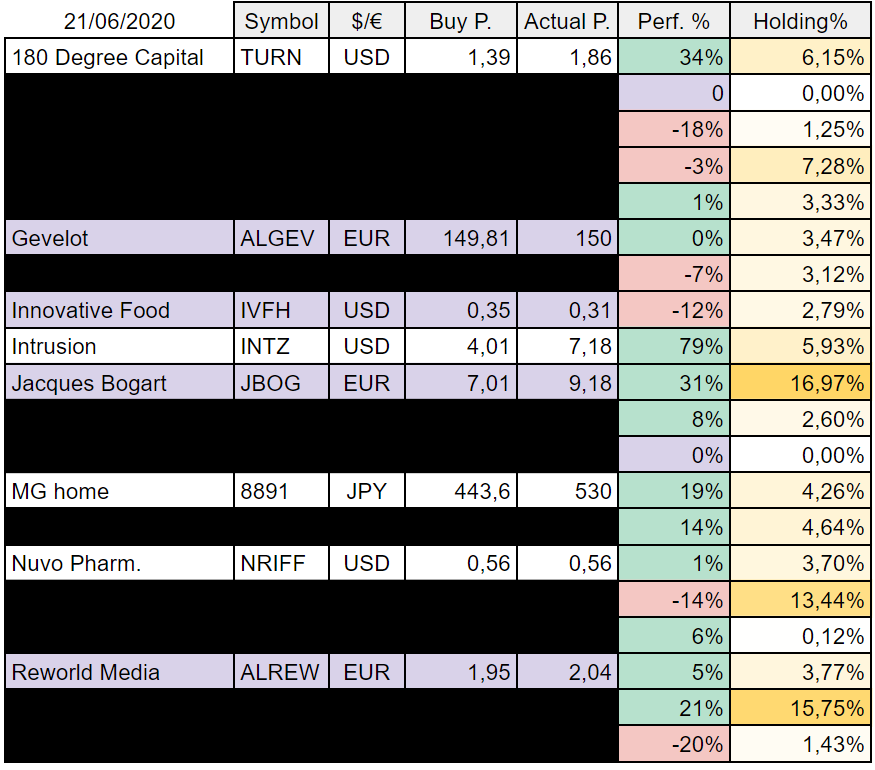

Current holdings

I sold MRVFF this week cause of the last quarterly report with an important net lossand bac expectations over the next quarters.

Credit Intelligence is an Australian nano cap operating in debt restructuring and personal insolvency management in Hong Kong and since 2020 in Australia.

The company employs over 30 staff, including accountants and legal practitioners, who work with financial institutions to provide creditors and debtors with customised cost-effective debt solutions. The company is benefiting from bankruptcies and from hard economic environment. The thesis here is simple : COVID crisis should accelerate its already fast expansion.

Financial ratios

Market Cap (USD) = 32.6M

Price to Book = 4.2

Price to Sales = 2.7

EV/EBITDA = 5.9

PER = 14

Revenue growth YoY= 127%

Quarterly revenue growth = 132.6%

Net cash = 2.44M

Debt/Equity = 22.31

ROE = 41.3%

ROA = 15.8%

Price/Free Cash Flow = 9.8

Chart

Nothing to say here, this google chart isn’t very readable.

Growth vs Dilution

We can see that despite the growth in revenue, the dilution is moderate.

The company purchased two companies in 2020 :

In July 2020 : Chapter Two Holdings Pty Ltd (CTH), a Sydney based debt negotiation business.

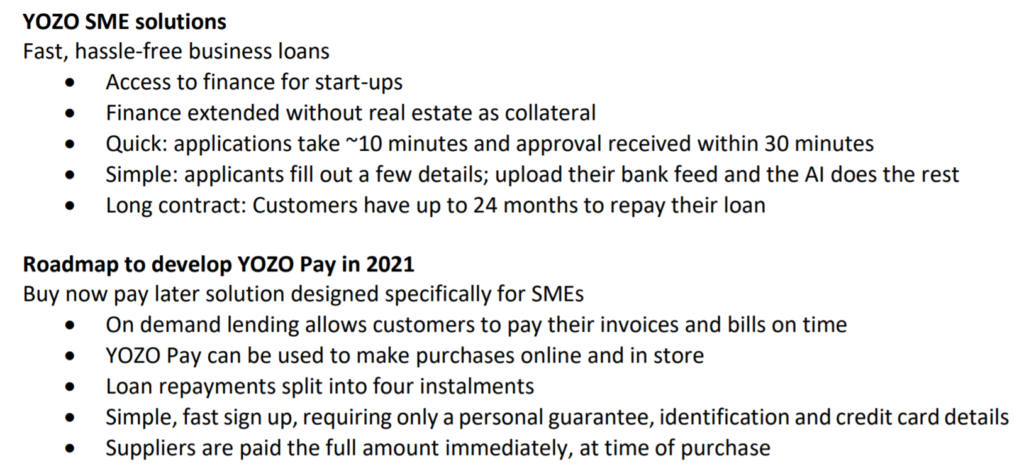

In December 2020, it acquired 60% of Australian fintech YOZO Finance Pty Ltd, a company that synergies well with Chapter two and will help the company to continue its grow through two offers :

These two acquisitions should help to maintain the current growth. The little red flag is that the last acquisition will have a diluting effect : “consideration of $1.38, 50% in cash and 50% in CI1 shares (subject to 6-month escrow), was paid for 60% of YOZO”.

FitLife Brands is a US company specialized in nutritional supplements. The company sells its products through a partnership with the GNC franchise and online (ebay, Amazon).

The company has a strong growth but might encounter an issue due to the recent GNC bankruptcy (June 2020). Regarding the Q3 results, the management surprisingly announced that the bankruptcy shouldn’t have an impact on the company and could even be a positive factor. Here is the reason : “Almost all of the Company’s revenue from GNC relates to product sold in GNC franchise locations. As part of the bankruptcy process, GNC has announced plans to close a significant number of its corporate stores. While a small number of franchisees have also elected to close their stores as part of the bankruptcy process, the Company believes that the closure of a significant number of corporate locations may drive increased traffic to the remaining franchise locations, benefiting our franchise-exclusive brands.”

Financial Ratios

Market Cap (USD) = 15.4M

Price to Book = 3.32

Price to Sales = 0.83

EV/EBITDA = 6

PER = 6.6

Revenue growth YoY= 14.7%

Debt/Equity = 14.7

ROE = 17.5%

ROA = 56%

So we have a micro cap with strong ratios considering the year over year revenue growth.

Chart

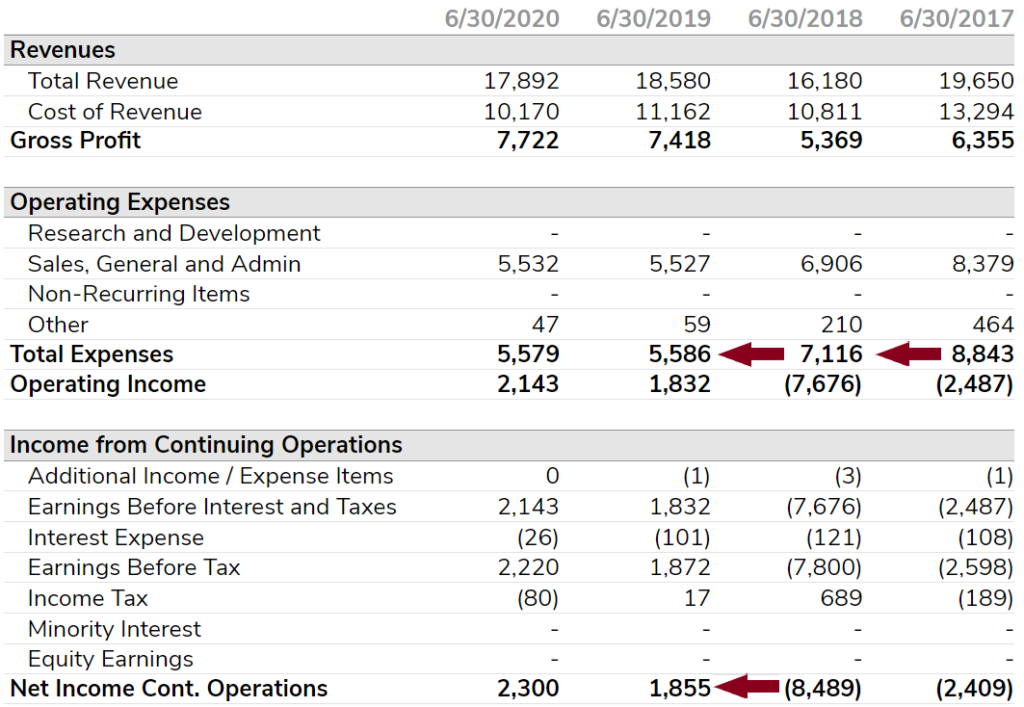

A good recovery chart, 2018 is the year corresponding to a cut in expenses. (see below)

Results

In 2018 and 2019 the management cut the expenses, this resulted in a positive net income while revenues stayed the same.

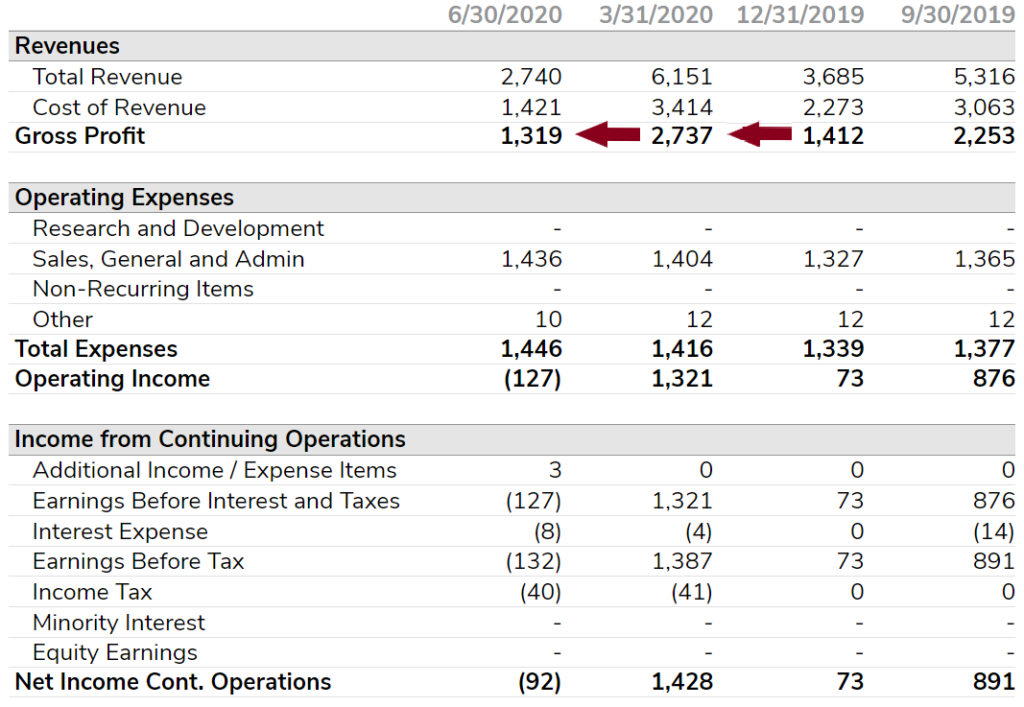

On the last quarterly results we can see that the COVID-19 impact was important but that revenues were almost the same as Q3 2019.

What do we expect in the future?

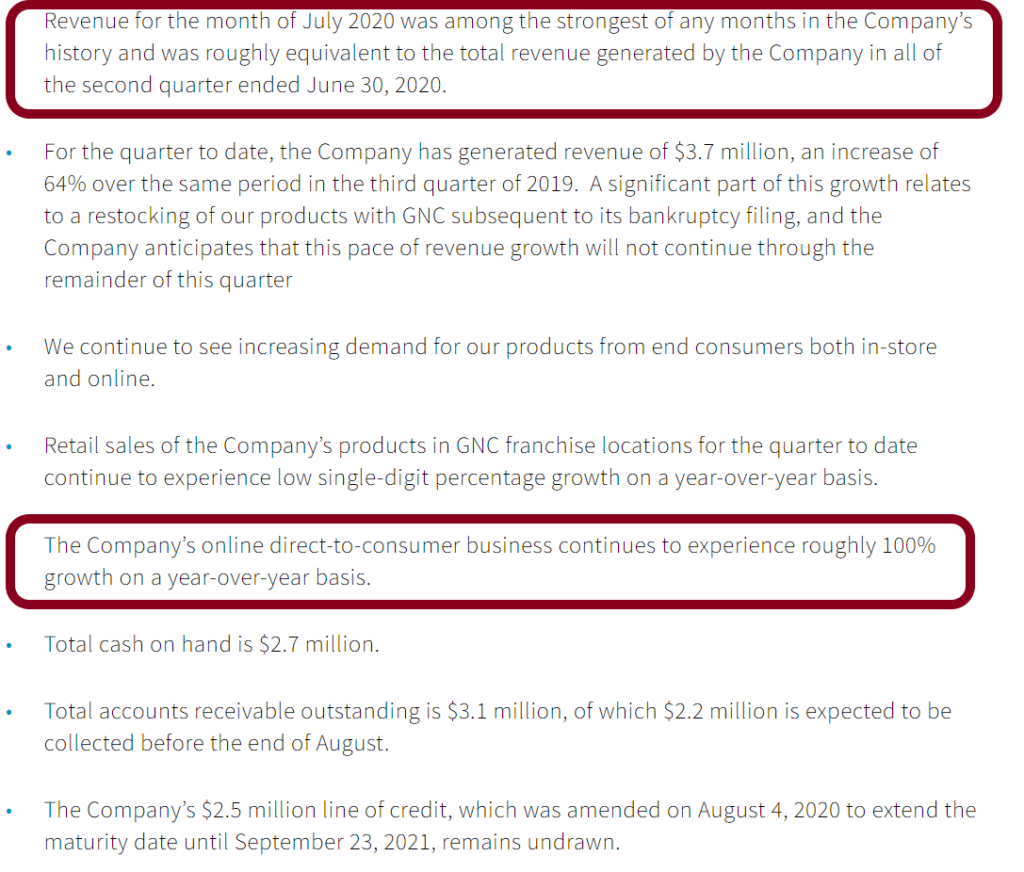

We expect that the growth will continue as mentioned in the August press release where I underlined two very importants points :

Looks like the July revenues are pretty encouraging for the future!

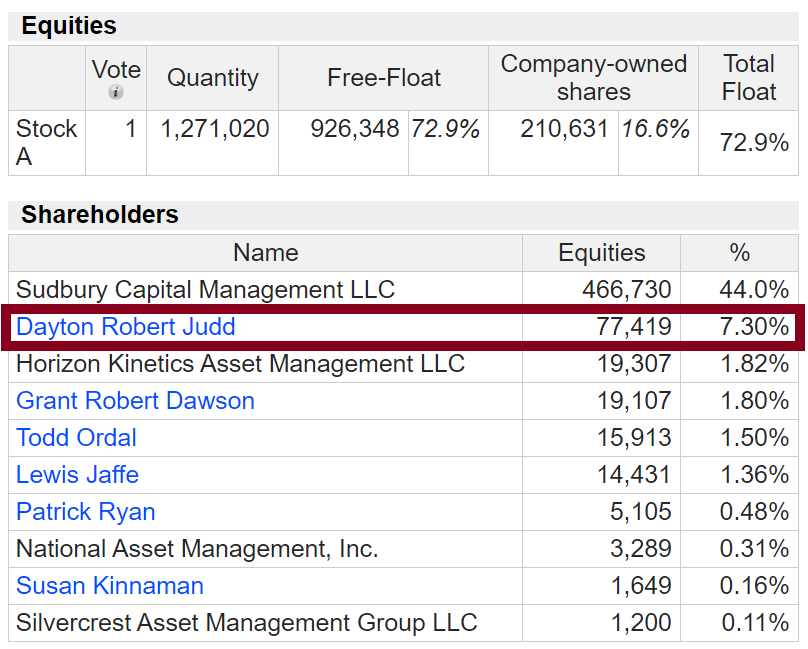

Shareholder structure

Using the MarketScreener website information we can see that the CEO owns 7.3% of the shares, he stopped buying in 2019 at $9.75. However, SudBury Capital Managment is also owned by Dayton Judd, meaning that he owns 51.3% of the company.

CEO’s interests should therefore be aligned to the ones of the shareholders, even if it wasn’t always the case in the past (see the good Seeking alpha article from here or in pdf below). This article is very interesting and will bring you more depth in the recent history of the company.

Disclosure : Long FTLF, I bought shares in May at $10.51.

Bonus

This is my current Portfolio. We can notice my first (and fast) 2,5-bagger with the rally of Intrusion caused by a potential huge contract (dig into their last Press release if interested).

Credits : OTC Market, Seeking Alpha (article written by Maarten Pieters whom I recommend to follow for his nice analysis), MarketScreener.

Gevelot is a French company operating in oil and gas industry. This company is profitable, it’s still growing and it’s incredibly cheap (share price trades under net cash). The growth rate was even better a couple of years ago but the company sold one of its bigger branches (Extrusion) in 2017 (explaining the last rally towards 220€/share).

Financial Ratios

Market Cap (in EUR) = 117M€

Net Cash = 160M€

Price to Book = 0.58

Price to Sales = 1.11

EV/EBITDA = -2.1

PER = 13.34

Revenue growth = 10.3%

Debt/Equity = 6.2

The company has a negative EV and is profitable. Net cash is way superior to market cap. Debt is very low. That’s all.

Chart

Share price was stuck during two years and then plunged from 200 to 140€ during the COVID-19 pandemic creating a big discount over cash. The company management has announced in the last annual report that 2020 results will be impacted by the pandemic but the net results should remain positive.

Shareholders

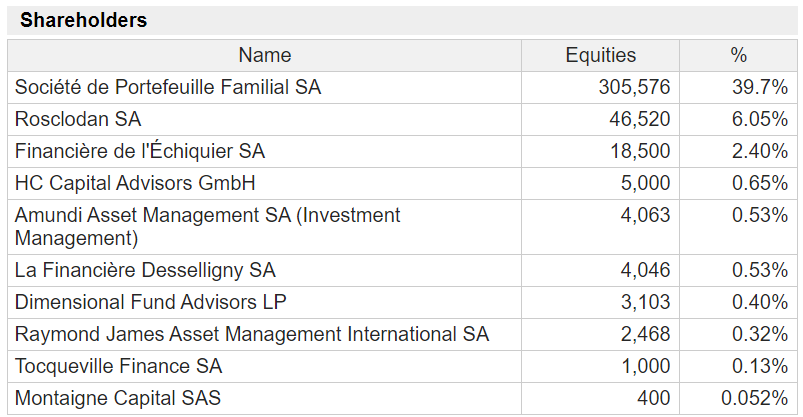

The company and its insiders don’t own any shares. More than 66% of the shares are controlled by SOPOFAM and ROSCLODAN and other societies.

-> The Marketscreener.com shareholder list seems currently out of date.

Catalysts / Risks

Possible catalyst: Takeover or Activism in order to take control of its net cash. The company could use its cash for acquisitions at a fair price like it did before.

Risk: Cash burn if the global conjuncture keeps deteriorating (e.g. a second COVID-19 wave).

Con: As my wife pointed out, it doesn’t seem an eco-friendly business.

Conclusion

The company is profitable and it’s quoting under net cash. The upside potential seems limited but we have a good margin of safety.

-> Bought at 149.8€.

My objective is 200€/share, which is still under Net cash/Share.

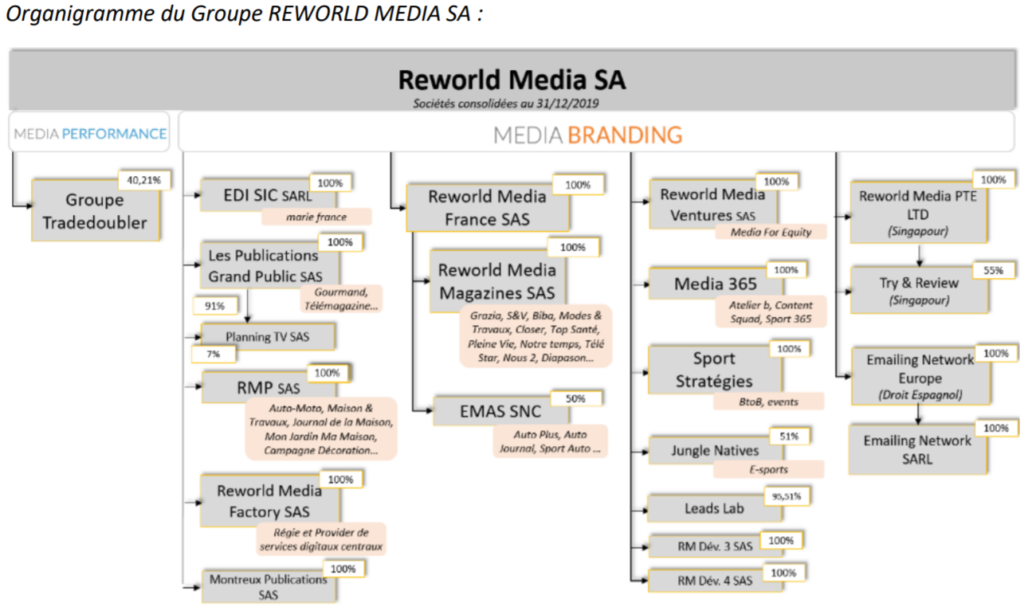

Reworld Media is a French company specialized in press and digital thematic media. It’s ranked as 1st thematic press publisher and 4th digital thematic media in France. The company was founded in 2012 and acquired many famous press brands since then. Some of its famous magazines are Closer, Marie France, Science & Vie, Grazia, Auto Plus, Télé Star.

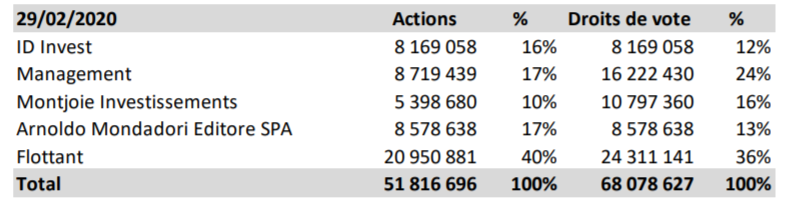

The float is about 40% and the management owns 24% of the company.

Financial Ratios:

Market Cap (in USD) = 117M

Price to Book = 1.2

Price to Sales = 0.34

EV/EBITDA = 2.53

PER = 3.97

ROIC = 16.8%

Debt/Equity = 99.5

FCF negative

-> So pretty solid ratios but a negative FCF and a debt level to monitor.

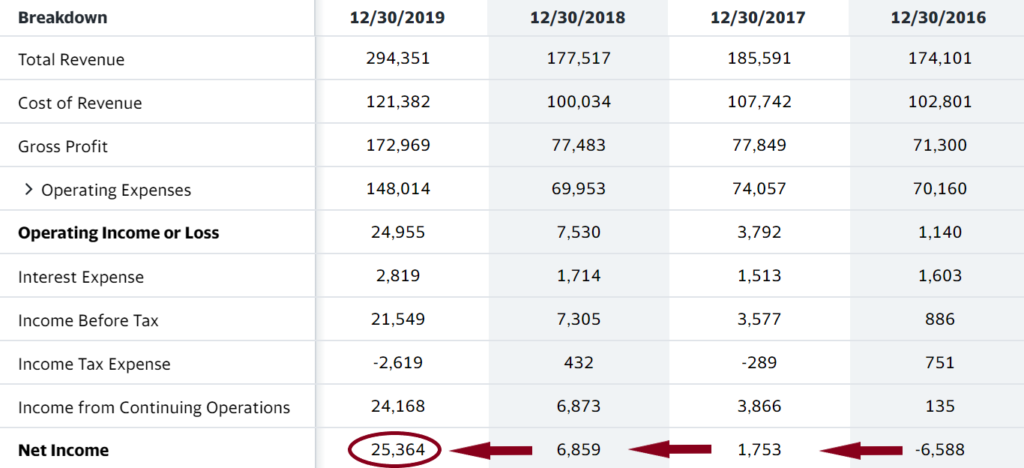

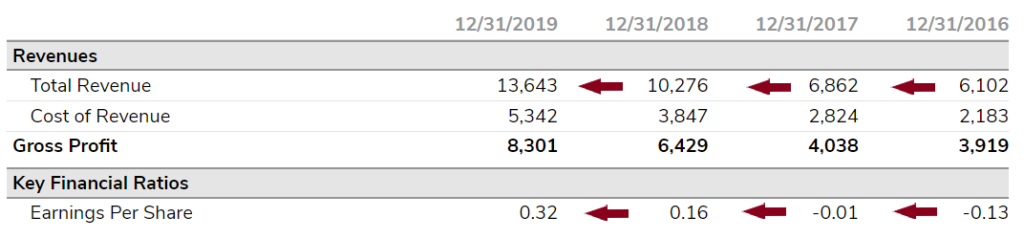

Let’s check the last financials statements :

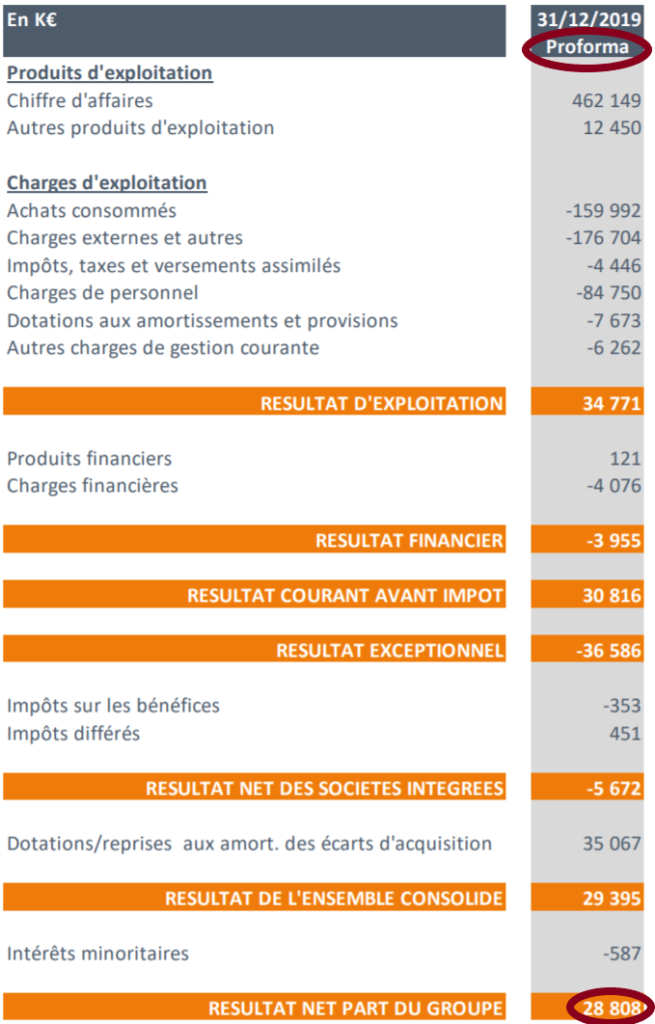

What a boom! But why? Well the last year revenue surged thanks to the 2019 acquisition of Mondadori France (a French division of an Italian Media group). The Pro Forma results are below :

These results are still pretty good and should provide good return over the long term. The Mondadori France acquisition was financed with a 93.3M€ debt and with share dilutions of 10M€ (April 2019) + 12.6M€ (December 2019). The company also bought football.fr and sport.fr in late 2019.

Chart

In 2012 share price was 0.05€ 😮

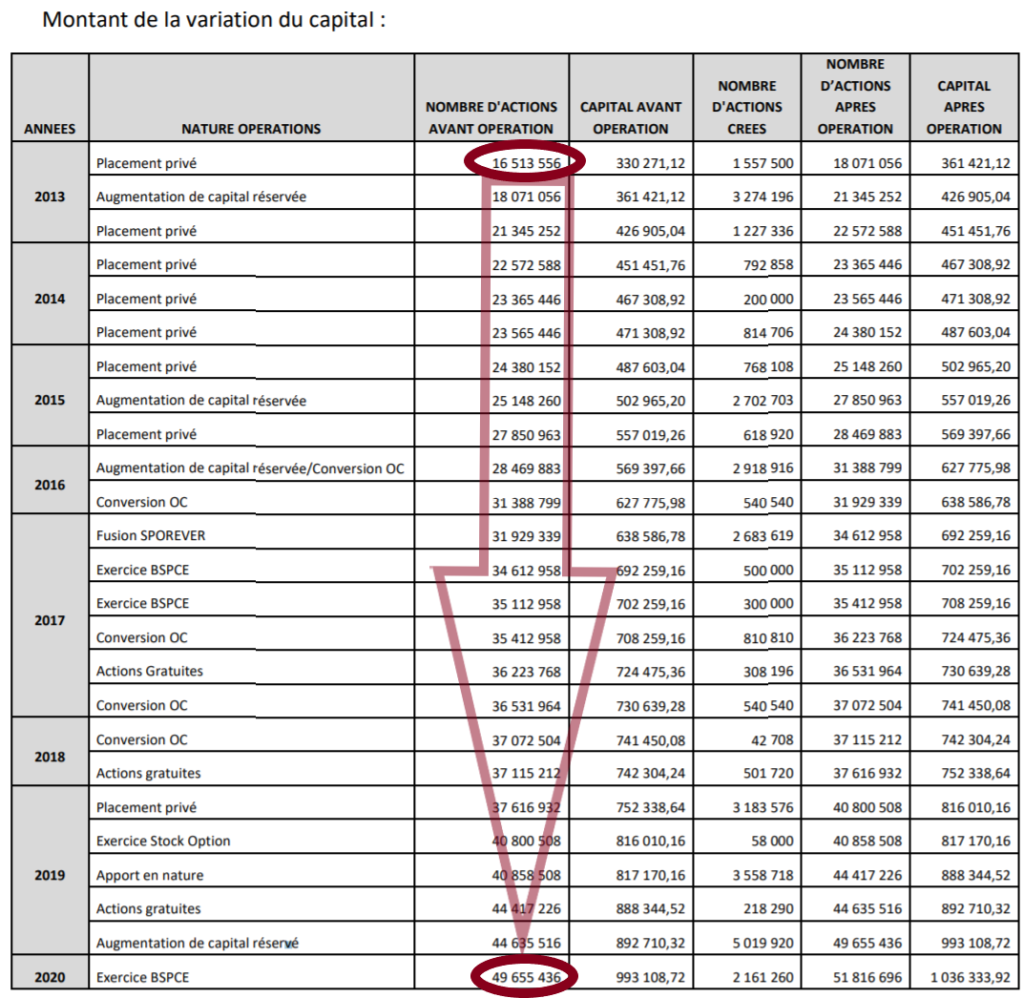

Now let’s take a look at the main thing: over the last 7 years, the total number of shares has more than tripled through capital augmentations. I have to confess I discovered it after I had already bought it… Such a mistake… but oh well now I know I have to check it before buying.

Company Holdings

Reworld Media owns 40.2% of Tradedoubler, a Swedish company (operating in various countries) whose market cap is USD13.8M, representing 1.8*0.4 = 5.55 Million USD. I didn’t find any information about the others companies owned by Reward Media since they all seem private.

COVID Impact

In March 2020 the company announced they had doubled audience on their sites with 40% more time spent on their sites.

Conclusion

We have a fast growing and a fast expanding company using debt and dilution to expand. Last year results were very good. Let’s summarize the pros and cons:

Pros : fast growth (growth rate highly superior to PER) and dynamic industry. The company is switching towards a digital audience and its size increase should allow it to make some savings on physical press. The Covid impact should be moderate or even a good point for the company. People staying at home means more people spending time on internet and reading journals in general. The company launched various online subscription offers during the pandemic, this could increase its future audience and thus its revenues.

Cons : The future of paper press is uncertain. Dilutions could be possible in the future (you could even remove the term “possible” since dilutions happened every year since 2013) and might not be compensated by growth.

It might be speculative but the company is still growing well and the future of digital press is promising.

-> Bought at 1.95€.

Disclaimer : This analysis is just my own opinion, I’m not a financial advisor, I did my own research that might have flaws.

Intrusion is a US company specialized in cyber-protection. It provides various softwares related to entity identification, data mining, cyber-crime prevention and advanced persistent threat detection. Its clients are the US government (federal + locals entities), banks, credit unions and other financial institutions, hospitals and other healthcare providers, and many more.

The company was founded in 1995 and is located in Texas, it currently has 32 employees.

Financial ratios :

Market Capitalization (USD) = 71M

Price to Book = 49.42

PER = 28.00

EV/EBITDA = 21.32

Growth rate Year over Year = 33%

Debt to Equity = 50

So we have a growth rate > PER (like Peter Lynch likes) with a decent debt to equity ratio.

Pros and cons

Pro : Revenue growth rate and EPS.

Pro : Industry. Ransomware and hacking have become more frequent over the last years affecting hospitals and big companies. The market should become bigger and bigger.

Con : Valuation is high and the growth needs to keep up with the years. Q1 was impacted by covid with a decrease in revenues of about 50% year over year.

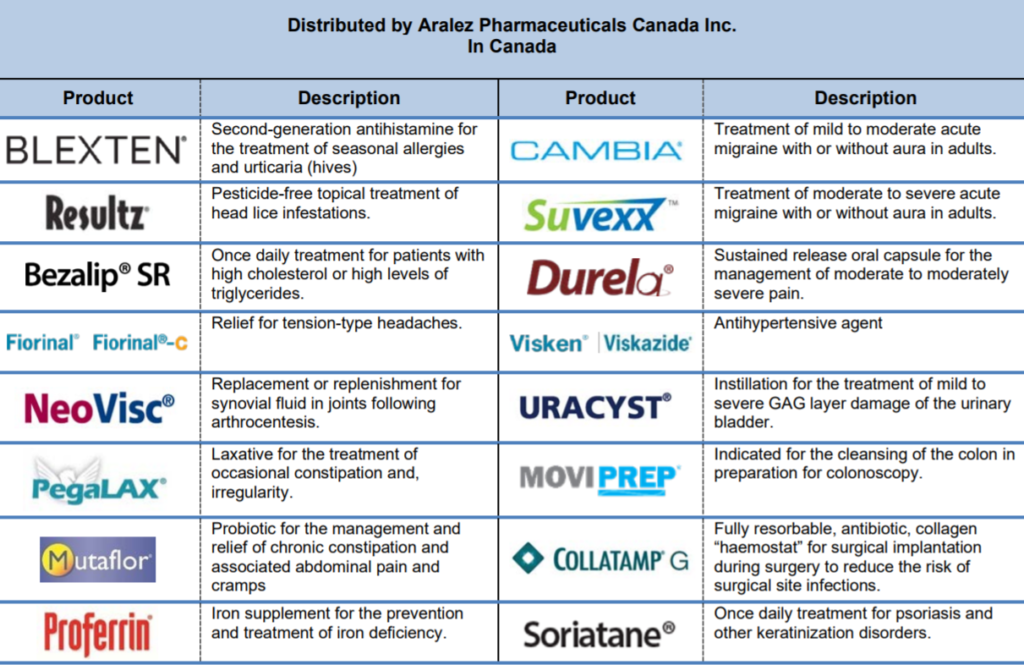

Nuvo Pharmaceuticals is a Canadian healthcare company specialized in pain, allergy and dermatological products. It’s a nanocap mainly selling its products in the US, Canada and Europe, and it’s recently had an agreement with Japan. Its main products are Blexten (antihistaminic), Cambia (anti-inflammatory) and Pennsaid (a local NSAID).

Here are some products/drugs they sell (Aralez Pharmaceuticals is owned by Nuvo, see below):

The stock is listed on two places :

OTCQX Market (USD) under the symbol NRIFF;

Toronto Stock Exchange Exchange (CAD) under the symbol NRI.

The company is a nano cap with a high growth potential, let’s take a look at its financial ratios (using USD 0.57 per share, and 2020 Q1 results):

Market Cap (in USD) = 6.2M

Price to Book = 0.4

Price-to-Sales = 0.38

EV/EBITDA = 2.2

PER = negative

And using the last annual report we have :

Revenue growth Year over Year = +267%

ROIC = 12%

Price/FCF = 0.75

So the stock is super cheap and revenue is nicely growing BUT debt level is high (see below).

Growth

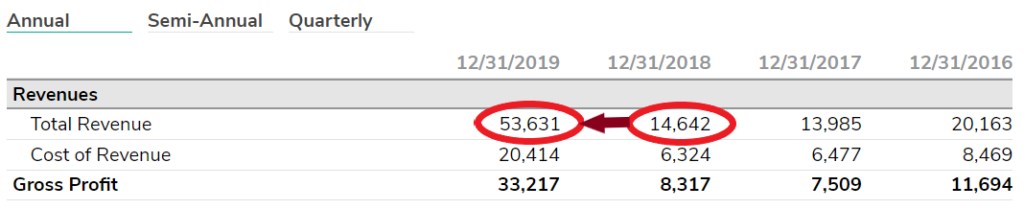

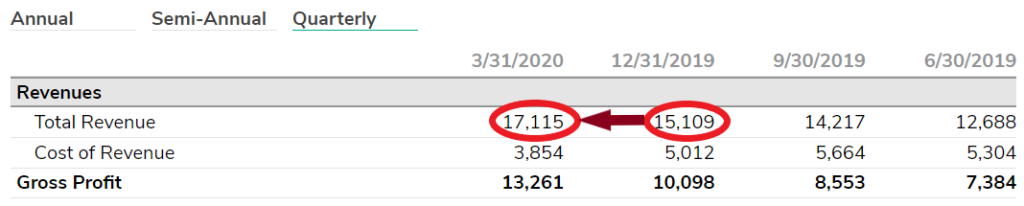

The reason that brought me to this company is the massive increase of revenue last year:

The growth was confirmed for Q1 despite COVID-19. We can notice the Q1 revenue surpasses 2018 full-year revenue:

The management seems to be confident about the future, the prescription of their drugs increased and they wrote in Q1 report about Blexten and Cambia: “Revenue related to these products was $6.0 million, an increase of 94% compared to revenue of $3.1 million for the three months ended March 31, 2019. Canadian prescriptions of Blexten and Cambia increased by 54% and 30% respectively compared to the three months ended March 31, 2019.”

Net income was USD 0.12 per share for Q1 2020.

We can read in the annual report that the 2019 growth was attributed mainly to one acquisition: Aralez Pharmaceuticals (the last owner of Blexten and Cambia). The acquisition cost $110M and was financed as follows:

6-year $60M 3.5% p.a. interest

18-month $6M 12.5% interest

52.5M convertible into 19,444,444 common shares of the company at a conversion price of US$2.70 + 25,555,556 common share purchase warrants, each such warrant initially exercisable for one common share of the company for a period of six years from the date of issuance at an exercise price of $3.53 per share.

Here are the advantages of the deal as described by the management :

Immediately and significantly accretive to revenue and adjusted EBITDA

Revenue diversification from product sales and royalty revenues

Provides Canadian platform with national sales infrastructure and an ability to launch and commercialize additional products

Significant cash flow from U.S. and international royalties of global Vimovo® sales

Low-cost financing from Deerfield Management Company, L.P. (Deerfield)

So the company has to reimburse a big debt but this acquisition seems worth it with the increase of Blexten and Cambia revenue.

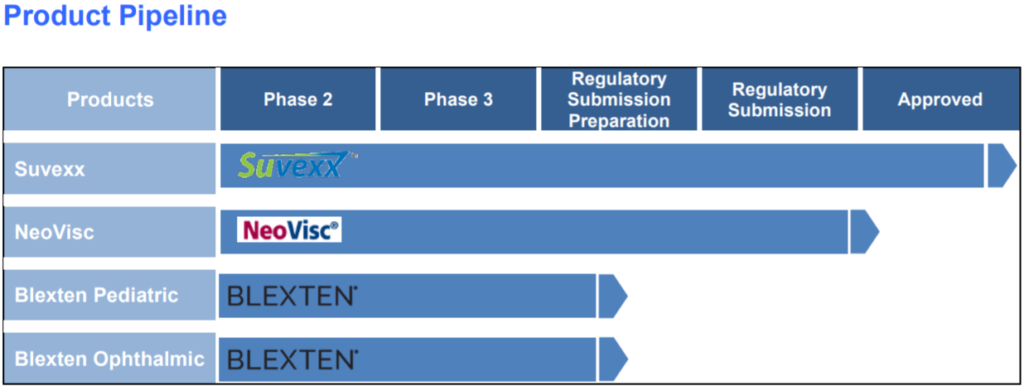

If you read the Q1 report you will notice the expansion keeps going: some of their drugs have recently been accepted in Switzerland and Japan and others are on the way to being approved by Health Canada.

Graph

We are close to a 5-year low, the market didn’t react that much to the revenue increase:

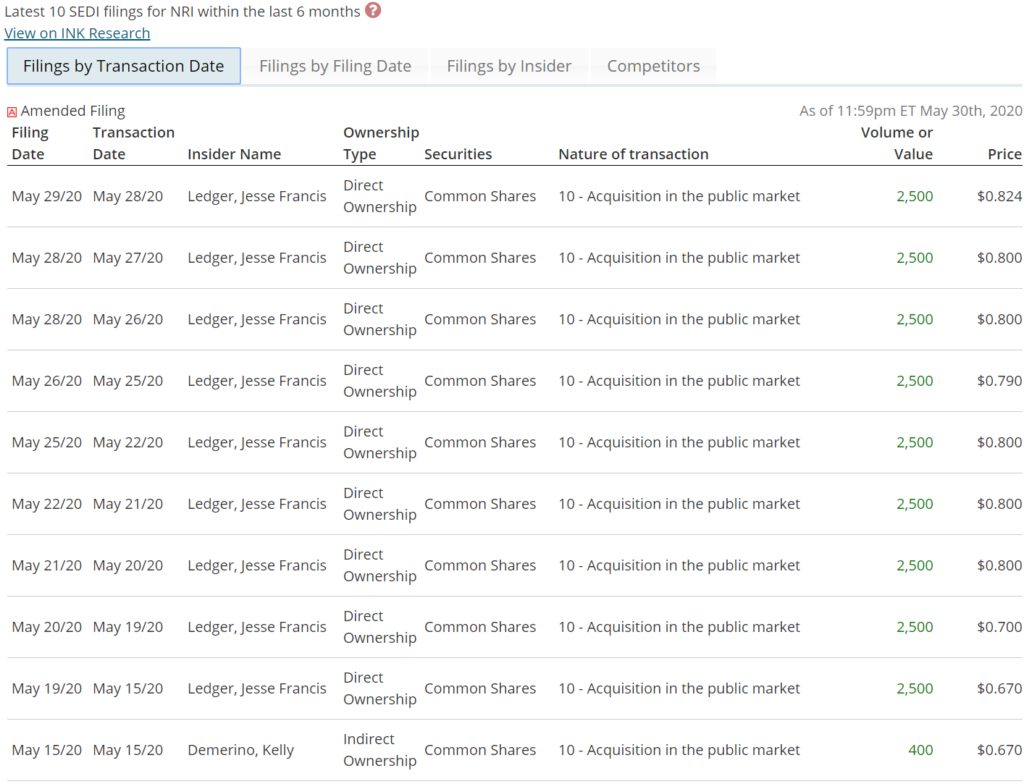

Insider Activity

Mr Ledger is the CEO of the company, we can see he has been buying shares in small amounts these last days:

The impact of the COVID crisis should be limited as the company is still running during the pandemic. This is what management wrote about it :

The Company is proactively managing the COVID-19 pandemic. The Company operates as an essential business, as defined by both the Ontario and Quebec governments. As such, the Company has made changes to operations to ensure our employees are safe and healthy, while the business continues to operate, including supplying global partners, wholesalers, pharmacies, and ultimately patients, with our healthcare products.

Conclusion

Pro : Nice growth perspective, low valuation, huge upward potential.

Cons : Debt, Debt and Debt. If the company cannot maintain its growth rate (and people stop buying their products), dilution could happen or worse.

A little tip: if you’re planning to buy it, you can do some arbitrage (it’s a nano cap, the price isn’t fairly balanced every time). Check the stock price in CAD or USD then convert into the other currency and choose the lowest price.

Jacques Bogart is a French company specialised in the design, manufacture and marketing of luxury perfumes and cosmetics. It sells some famous brands like Chevignon, Ted Lapidus, Carven, and its own brand Jacques Bogart.

The company sells mainly in France and Germany though physical stores but it’s also present in Israel, Belgium and Luxembourg. It has recently made some acquisitions that led to its expansion, the biggest one being Distriplus in the end of 2020.

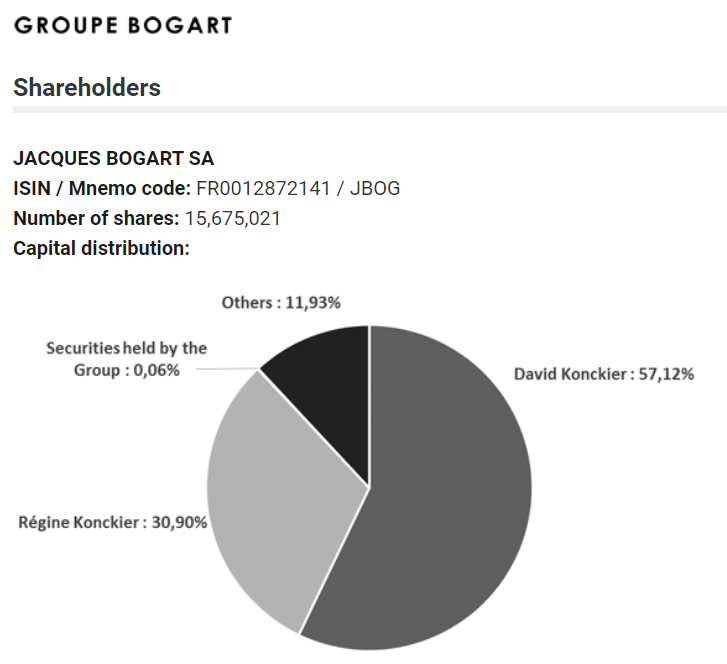

The company has a low float and it is mainly controlled by the Konckier family. Under the French law Loi Pacte if a shareholder owns more than 90%, the company can go private with shares being purchased at a premium price (remember this point!).

Let’s now take a look at the current ratios :

Market Capitalization : 110M€ (USD120M)

Price to Book = 1.17

PER = 8.06

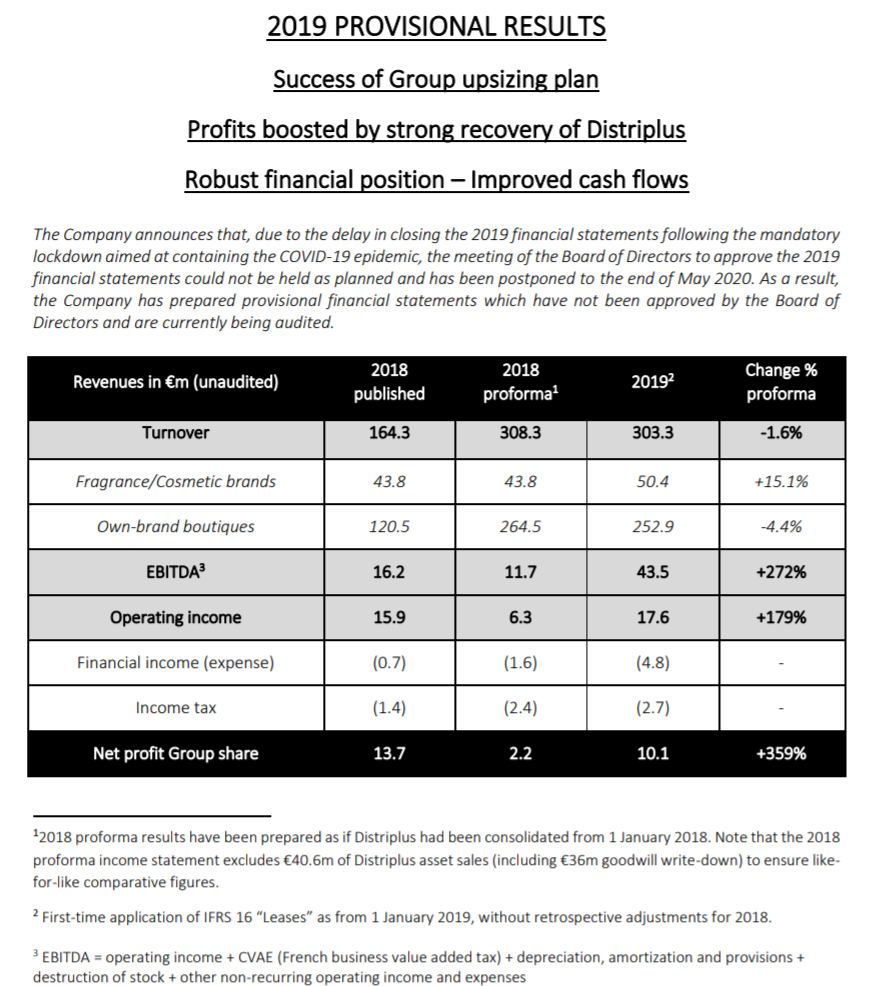

I didn’t post others ratios because we don’t have a full financial report for now. However, we have this :

EBITDA increased by more than 2.5x last year! All of this despite Distriplus being operational for only several months in 2019. So before COVID perspectives were very good.

For FCF, the last press release mentions a nice increase:

Other financials ratio are ok and the company secured cash before the crisis (and still plans to make other acquisitions if given the opportunity).

We can notice that the big drawdown due to COVID has not yet recovered:

COVID Impact

We don’t know how exactly the current crisis affected the company; here is what management said about the COVID impact in the last press release:

Insider activity

Remember the Konckier Family owns 88% of the company and a 90+% ownership of a company means that the company can go private with shares being purchased at a premium price.

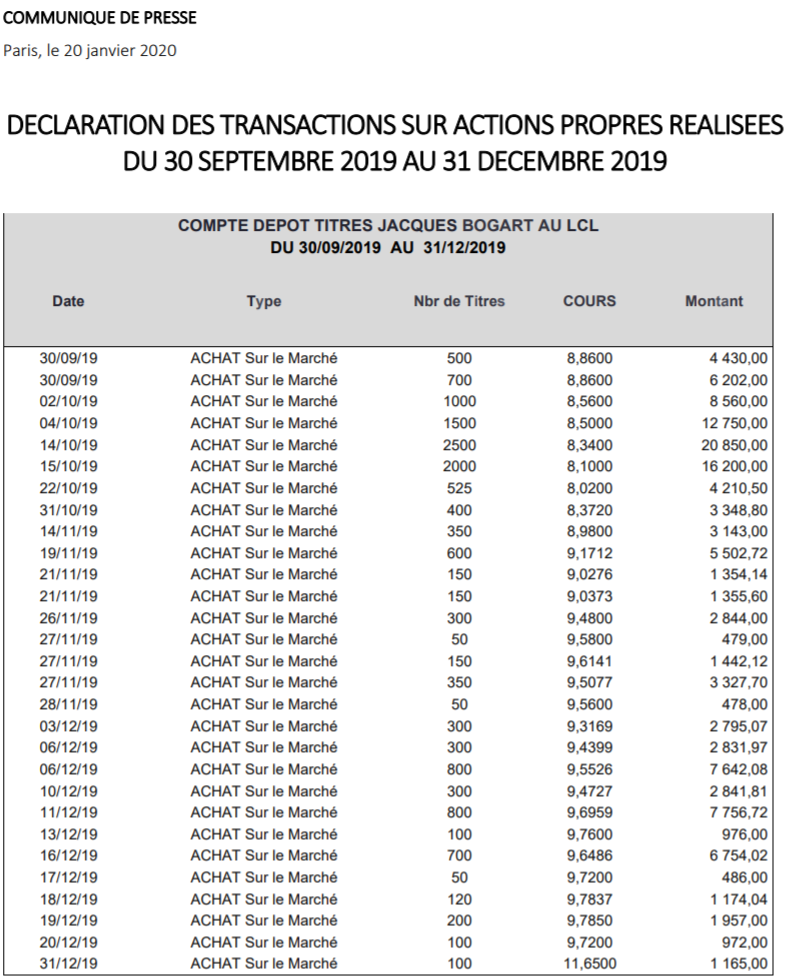

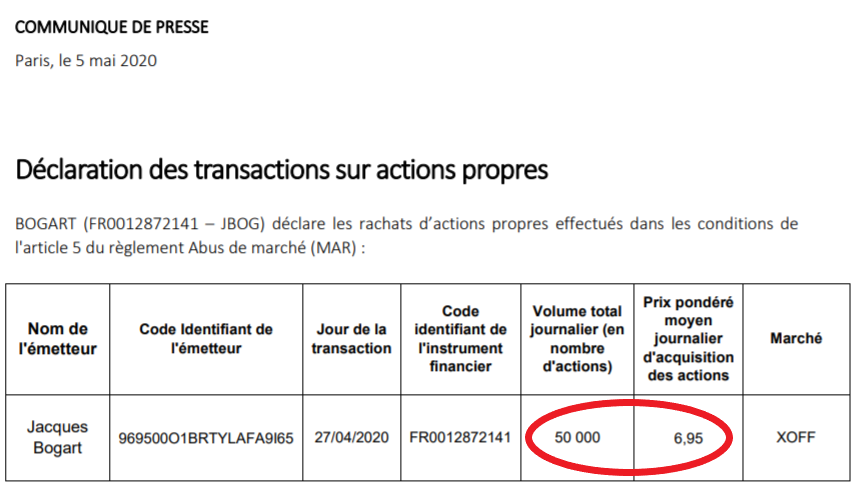

The company bought back its own shares from September to December 2019 as follows:

We don’t have data about early 2020 except this:

With this big transaction, the Konckier family now probably owns more than 90% of the shares, allowing them to turn the company private.

Conclusion

What am I expecting with this stock? Well there are two options imo:

Family Konckier will ask to turn the company private if they now hold more than 90% of its shares -> they will have to offer a good price to its shareholders.

There will be no private mutation but the company will keep growing given the current cheap valuation.

Risks : If pandemic continues and there is a second wave, the closing of stores over the long term can damage the company revenues.

-> Long, purchased at 7.00€

It’s almost the same price of the last buyback: it adds a little security to the investment (if they bought it at this price it probably means it is not overvalued).

IVFH is a nano cap operating in the food distribution area. The company consists in a holding of different food related companies. Here are some of its holdings :

Food Innovations : management of artisanal food delivery directly to chefs ;

Gourmet Foodservice Group : a food delivery for professionals ;

Some websites of food delivery : igourmet.comspecialized in cheese, mouth.com specialized in food gifts (as an old domain name trader I can appreciate the underlying value of “mouth.com”).

I found the company browsing the OTC Markets website and stopped because of these ratios (calculated with $0.35/share) :

Market Cap (in USD) = 12 Million

Price to Book = 1.18

EV/EBITDA = 4

PER = 11.5

ROIC = 14%

FCF yield = 25%

Debt/Equity = 11.6

…associated to a revenue grow of almost 20% per year in the last 5 years!

So what’s the catch?

The number of shares outstanding has been stable over the last years, the company is active and it communicates well. Well I don’t find the catch!

The COVID crisis seems to be having a moderate impact on the company, here is the statement of the CEO Mr Klepfish (he owns 5% of the company) on 24th March :

“We are currently experiencing surging ecommerce sales at igourmet.com and mouth.com for a variety of specialty food categories including higher demand for themed food kits. Simultaneously, ecommerce sales have significantly accelerated for our specialty grocery products offered through our other online channels including amazon.com and walmart.com.

Strong direct-to-consumer sales are partially offsetting reduced specialty foodservice distribution revenue experienced as a result of the affects the COVID-19 pandemic on the restaurant, travel and hospitality industries. Based on current information, we expect our cash balances on hand, plus availability under our existing credit line, to provide sufficient liquidity to manage the business, while supporting the surge in ecommerce demand. As part of our multi-channel distribution strategy, we have continued to expand our platform to serve evolving specialty food buying trends. We anticipate a continued shift towards ecommerce channels and our unique food distribution model has allowed us to quickly expand our ecommerce offerings, while seamlessly adjusting resources and products from our foodservice business to keep up with recent specialty grocery demands.”

So it’s ok for me, the company will survive + it can expand targeting new consumers and should continue to grow. The company has low debts, which is nice during these hard times.

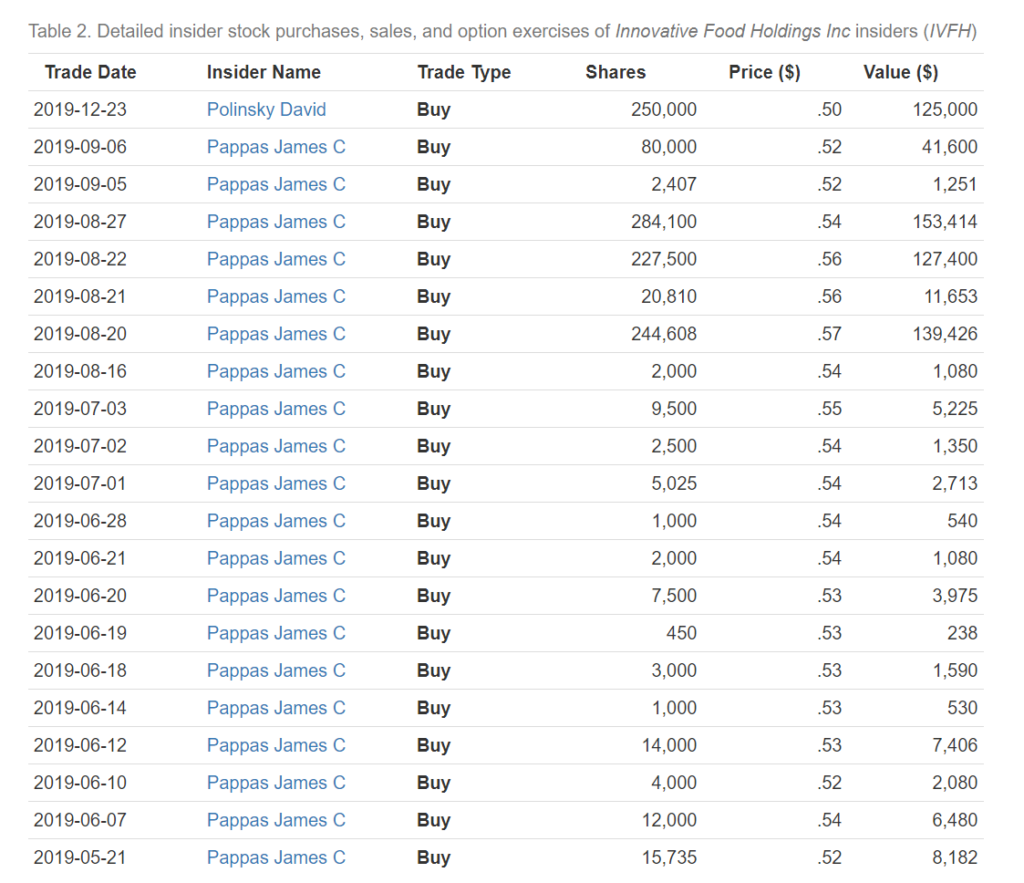

Let’s have a look at insider activity :

No new trades in 2020 were reported, but amounts purchased in 2019 are fine.

-> I purchased shares at $0.35.

Disclaimer : This analysis is just my own opinion, I’m not a financial advisor, I did my own research that might have flaws.

Edit May 17th, 2020

The company published its 10-K and exposed COVID effects on its sales.

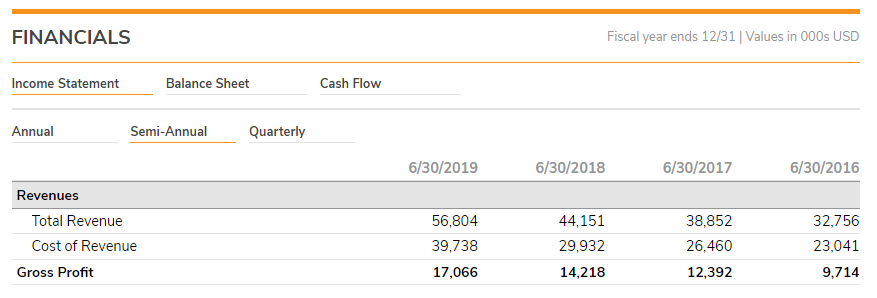

Total revenue increased 9.4% to $57.9M, compared to $52.9M in 2018, a much lower percentage than for 2018/2017 were it surged 28%. Net revenue per share is $0.01. FCF is negative this year, cash level is $4M compared to $4.8M last year.

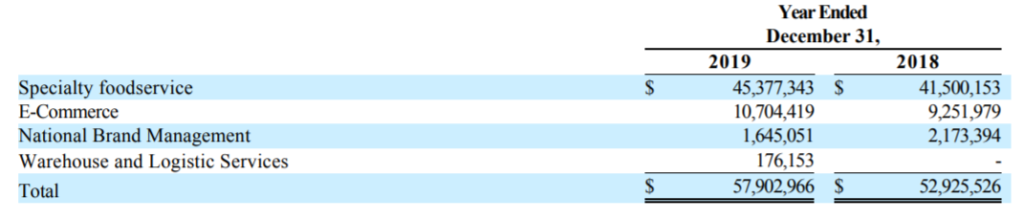

Here is the revenue repartition per activity :

Specialty foodservice : considering it refers to restaurants deliveries and co. we can see it represents majority of income. COVID crisis impacted this source of revenue but we do not know how much.

E-Commerce : management highlighted the huge growth of online sales during epidemic : “e-commerce orders surged in March and April and increased over 150%, and over 400%, respectively. “ ; “e-commerce customers in April were over 31,000, an increase of over 290% over the prior year period”. The company put resources inside e-commerce “We quickly pivoted foodservice resources and products to direct-to-consumer offerings, while launching new products developed by our e-commerce teams specifically tailored for the current market environment”. Let’s hope this turn will be enough for maintain the current grow and will compensate foodservice revenues.

For conclude I’m a little bit disappointed by these results but if e-commerce turn works well and consumers still there after end of lockdown it should compensate lost of revenue of traditional foodservice domain.

MG Home, is a Japan based company selling and leasing real estate. The company is a microcap stock quoted on NSE-2 (Nagoya stock Exchange) / TSE-2 (Tokyo Stock Exchange) and domiciled at Nagoya.

The company build, sell, lease and manage properties located around Nagoya at center of Japan. Nagoya the fourth biggest Japan city, his Metropolitan region is the third bigger and count 10.2 Millions inhabitant. This area locate headquarters of Toyota, Brother (the printer) and many automotive/ceramic companies.

41% of MG Home shares are owned by VT Holdings, an USD 300M market cap company operating in vehicle area (mainly selling Honda cars and repairing cars) listed on NSE-1 and TSE-1. I checked this company, I don’t think it’s worth to own MG shares through VT Holdings. Car companies will be severly impacted by COVID and we don’t have enough discount on asset there (P/B = 0.89).

On a valuation view MG home is incredibly cheap (using JPY432 per share) :

Market Cap (in USD) = 11.6 Million

Price to Book = 0.34

PER = 1.3

Price to Sales = 0.1

Price to cashflow : 1.24

EV/EBITDA = 2.9

ROE = 23%

Debt to Equity : 77%

Debt to equity ratio should be monitored over long term.

During last four years, sales and net income increased slightly :

This year we have (before COVID-19 crisis) :

-> Company still growing, financial statements of year 2020 will come on May.

Number of shares is stable since 2009 (with a stock split in 2015). A good point cause the company didn’t diluted his share but a bad point cause zero buyback were done. Some consolation can be found with a small dividend (JPY21) paid every year slowly increasing year after year.

Some graph chart to complete analysis :

I’m not a big fan of chart analysis but we can see a big drop during COVID crisis and an upward average trend since 2019.

COVID crisis may impact the business but lockdown wasn’t long in Japan and population is used to wear mask. It should limit the spread of infection. In Europe lockdown suscited the envy of population to move on countryside, a good point for MG Home if same thing happen in Japan.

My Objective = 1270/share (100% of Book Value per share). At this price if growth continue it still pretty cheap.

Disclosure : Long 2.6k shares, purchase price JPY443

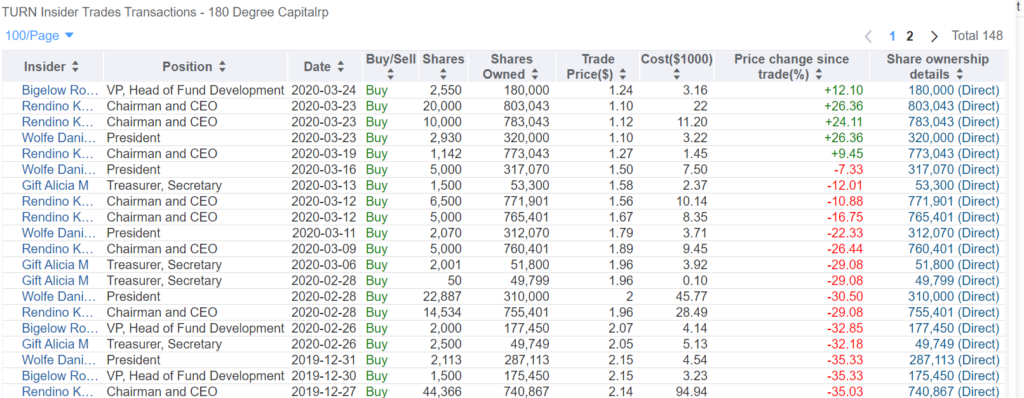

180 degree capital is a closed-end mutual fund discounting to his Net Asset Value. Discount was 30% in December, now it’s 55% based on pre-crisis portfolio valuation. It could be lower or higher depending on the portfolio performance during crisis. I didn’t check evolution of all public portfolio lines but below is the evolution of two of them. What we can see is they weren’t that much impacted by the virus:

Some metrics (using $1.4/share) :

NAV/Share = 3.06

Price/Book = 0.45

MarketCap = 40M

ROE = 15%

Insiders continued buying shares during crisis, none of them sold. They bought the bottom. A good sign telling me they are confident for the future.

Conclusion : A pretty decent discount, with insider buying and a decent manager focusing on micro cap activism. Impact of crisis is uncertain but the big discount protects us quite enough.

-> Long. Purchase price: $1.4.

Ah some fast news : I closed my short position and Softimat skyrocketed this week! Some purchases will come on next weeks. Cheers.

I didn’t write for many months, I will try to update my site more frequently.

I sold almost all my lines just before COVID-19 came to Europe. I went hardly short on February using 75% of my French portfolio on a double short ETF replicate (BX4). I anticipated this crisis using reddit and following reports of r/China_Flu so thanks Reddit (and a big shame to Twitter that censored all COVID hashtag from january to february).

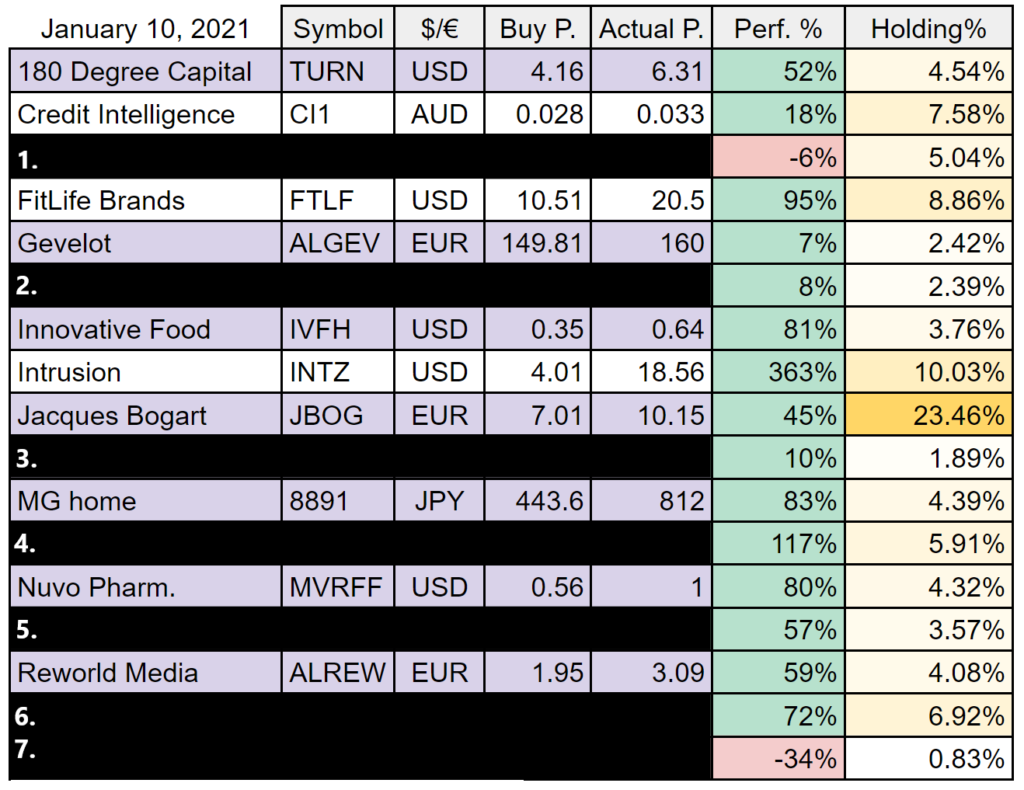

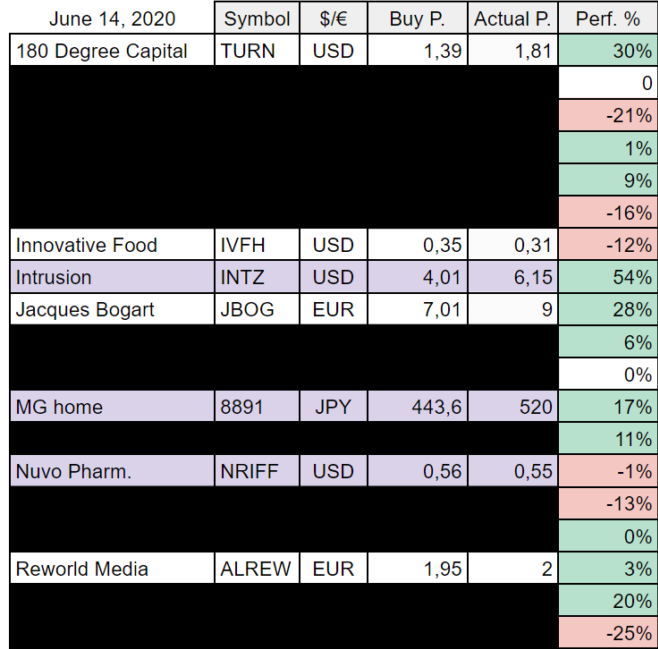

Here is my current portfolio :

BX4 (leveraged x2 short CAC40 ETF) purchased at 3.02€

Softimat purchased at 3.53€

MG Home (analysis to come)

Nisso Pronity (analysis to come)

I kept Softimat cause I have a big stake there and the stock is pretty illiquid + I think it won’t be as much impacted by COVID-19 cause of :

It has few number of employees that still can work from home ;

The society is a REIT, Real Estate is a protection from inflation if BCE print money as FED did ;

Buybacks continue during crisis (last buybacks on March 26 at 4€).

The only risk would be renters to stop pay their lease cause of bankruptcy, I have to conceed I didn’t checked who are the renters.

I will post a more in depth analysis about Softimat soon.

Now is the biggest challenge : when to exit short. Well I don’t know, I think crisis is front of us and not behind. I read on a twitter account (such scientific haha) that CAC40 net value is 3200, I won’t go under this price and it feel a correct take profit. I still don’t have stop loss, I don’t like them, I bet I exit if people restart to work, and if I find good opportunities with a better risk reward than my short. Japan is the first step, I have some companies I’m waiting to invest on.

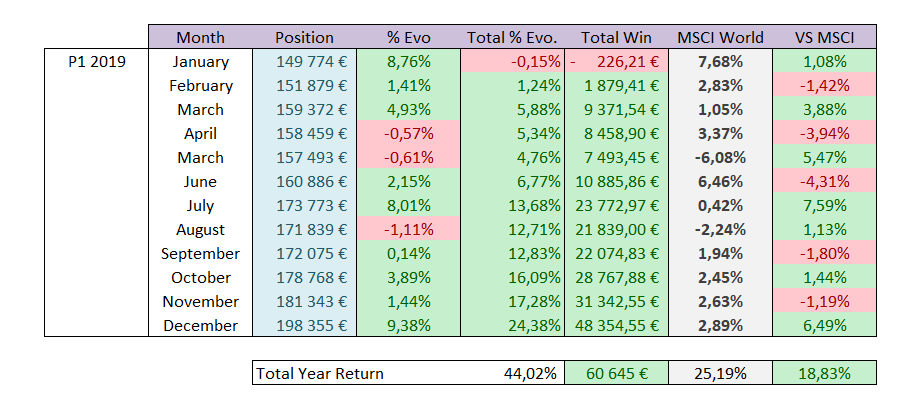

2019 was an excellent year with a 44% return on my main portfolio or a 60.6k€ net win. This portfolio is purely french (with one belgium holding exception), GRVO and GAM count for 60% of all holdings.

I started building my second portofolio during summer, and filled it completely in november. Results aren’t significative, I won 1k but lose on overall return percentage (my last positions were bigger and had better return).

Here is a view of my main portofolio evolution during 2019. I started 1st January 2019 with 137k€. I didn’t make deposit.

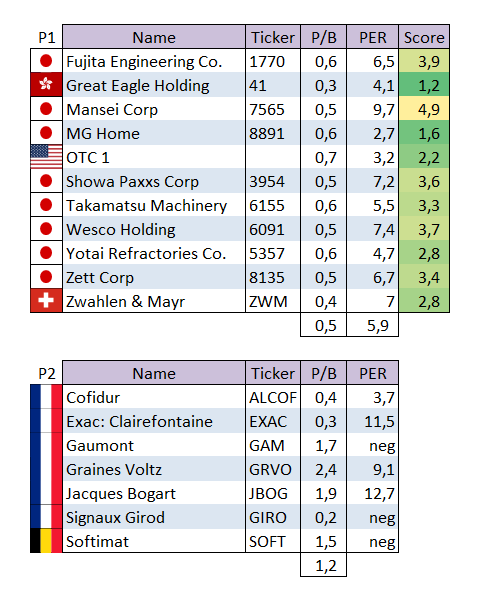

Here are my current holdings as to 01.01.2020 (P2 is my main portfolio) :